The Impact of Fed Rate Cuts on Franchises

The federal funds rate plays a massive role in determining borrowing costs for businesses and consumers. When the Federal Reserve lowers interest rates, it stimulates economic activity by increasing credit availability and making commercial and personal loans more attractive. This typically benefits businesses across industries, with capital-intensive sectors ideally positioned to grow.

We explored the impact of cutting interest rates on the franchise industry, which currently boasts over 820,000 franchise establishments in the US and is forecast to generate $893 billion in 2024.

What Is the Federal Funds Rate?

The federal funds rate is the interest rate at which banks lend reserves to each other overnight. It heavily influences other interest rates, including mortgages, personal loans, and commercial loans. The Federal Open Market Committee sets the rate (FOMC) based on its interpretation of macroeconomic data, such as consumer spending, the unemployment rate, job openings, and myriad other data points gathered by the twelve regional US Federal Reserve banks nationwide.

Why Raise Interest Rates in the First Place?

The US Federal Reserve has a dual mandate within the government. Its job is to ensure price stability and work toward maximum employment. The federal funds rate is the Fed’s most important tool in accomplishing these competing objectives.

- When economic activity is too high, it causes inflation, a potentially dangerous form of price instability. The Fed cools economic activity by raising the federal funds rate, increasing the cost of borrowing, and slowing the economy down. This also raises the risk of reducing business income, which causes increased unemployment, the Fed’s “other” job.

- When economic activity is too low, resulting in high unemployment, the Fed lowers the federal funds rate to lower borrowing costs and stimulate spending. This leads to increased labor demand, reducing the unemployment rate.

The Fed is responsible for maintaining a Goldilocks economy, where inflation remains around 2%, and unemployment stays near “maximum employment,” a term without a specific numerical definition. Even the Fed’s 2% inflation rate goal is somewhat arbitrary.

The Impact of Cutting Interest Rates on Franchise Business Loans

The most common business loan for franchisees is the SBA 7(a) loan, which typically covers franchise fees and other startup costs associated with starting a franchise establishment. As of 2024, SBA 7(a) loans are capped at $5 million, with most approved loans near the US small business loan average of $633,000.

As of September 2024, the current federal funds rate is 5.25% to 5.50%, pending a cut of 50 basis points. For comparison, the average interest rate for franchise loans (the SBA 7(a)), is nearly three times higher:

- 11.25% for loans over $50,000

- 12.25% for loans of $25,001 to $50,000

- 13.25% for loans of $25,000 or less

SBA 7(a) loans have repayment periods between 7 and 25 years, and the actual rates offered to businesses vary based on credit ratings, collateral, and other factors. In short, franchise loan interest rates are far more variable – that is, volatile – than the funds rate. For example, during the five years between Q2 2012 and Q1 2017, the average SBA 7(a) interest rate was 3,680% higher than the federal funds rate, or 465 basis points on average per quarter.

Of course, nearly all personal and commercial loan interest rates are considerably higher than the funds rate. This also means even slight changes of even 1 to 2 basis points have an exaggerated impact on broader lending rates. For example, mortgage rates fell more than half a basis point in anticipation of a 25 basis point cut in September 2024.

Rate Cuts and Franchises: A Matter of Timing

The Fed’s dual mandate requires constant rebalancing of priorities, which leads to cycles of changing fiscal policies. As economic activity declines, the Fed cuts rates or engages in fiscal expansion. When times are good, it may adopt fiscal tightening and raise rates.

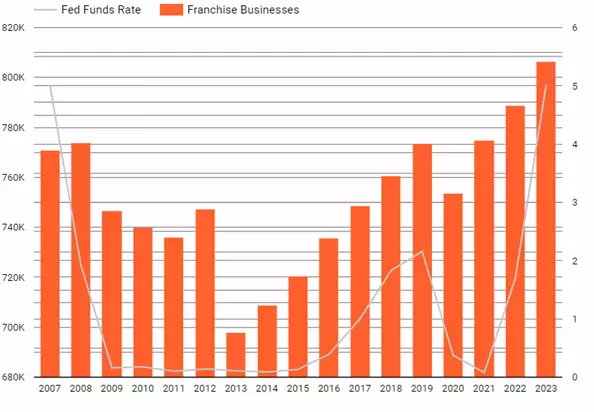

We looked at the average federal funds rate annually from 2007 through 2023, a period that included the financial crisis and subsequent Great Recession, the long recovery, and the pandemic-induced recession of 2020, to see what happens when the Fed cuts rates. The Fed lowered rates in six of those years. The number of franchise businesses increased in two of those years and decreased in the other four years.

During or after a recession, franchises have experienced two very different outcomes over the past two decades. The number of franchise businesses fell by 33,918 during the Great Recession and increased by 35,144 in the sub-1% federal funds rate environment that characterized the pandemic economy.

In these two cases, it appears the Fed may have waited too long to cut rates, or the franchise industry is more susceptible to rate volatility than other sectors. Changes in franchise businesses also vary widely by industry and geographic location, variables unaccounted for with existing FRED data.

Do Rate Cuts Help Franchise Organizations?

Based on this small data sample, we can say rate cuts help franchises in the long run but do not stimulate immediate growth. In most cases, franchises can expect a two- to three-year lag in growth after a rate cut.

One thing is clear, however. Sustained periods of low interest rates (under 3%) positively impact most businesses, including franchise organizations. In years with rates under 3%, the number of franchise establishments increased five times and declined three times. The gains during the sub-3% period were substantial, adding over 62,000 businesses in a single four-year span from 2013 to 2017, mirroring the broader economic recovery.

The Franchise Industry Is Kind of Our Thing

Oneupweb takes a lot of pride in being one of the most respected franchise marketing agencies around. We’ve earned that reputation by creating insightful strategies, delivering quality services, and learning the industry inside and out. From business models to mergers and acquisitions, we grow your business because we know your business. See what over twenty-five years of franchise industry experience can do for your organization; get in touch or call (231) 922-9977 to get started.